The AI search category has a data problem. Vendor decks quote adoption percentages nobody can trace, "studies" of thousands of queries nobody can inspect, and lift numbers with no methodology attached. For a discipline whose entire premise is that AI engines reward trustworthy sources, that's an awkward habit.

So this piece holds itself to a stricter standard: every number in it is third-party, named, dated, and linked. No first-party survey, no proprietary corpus, no composite. Just the published record as of June 2026, and what it adds up to.

It adds up to three findings. Adoption is settled. B2B got there first. And the metric marketing teams spent twenty years optimizing no longer describes how buyers behave.

Key takeaways

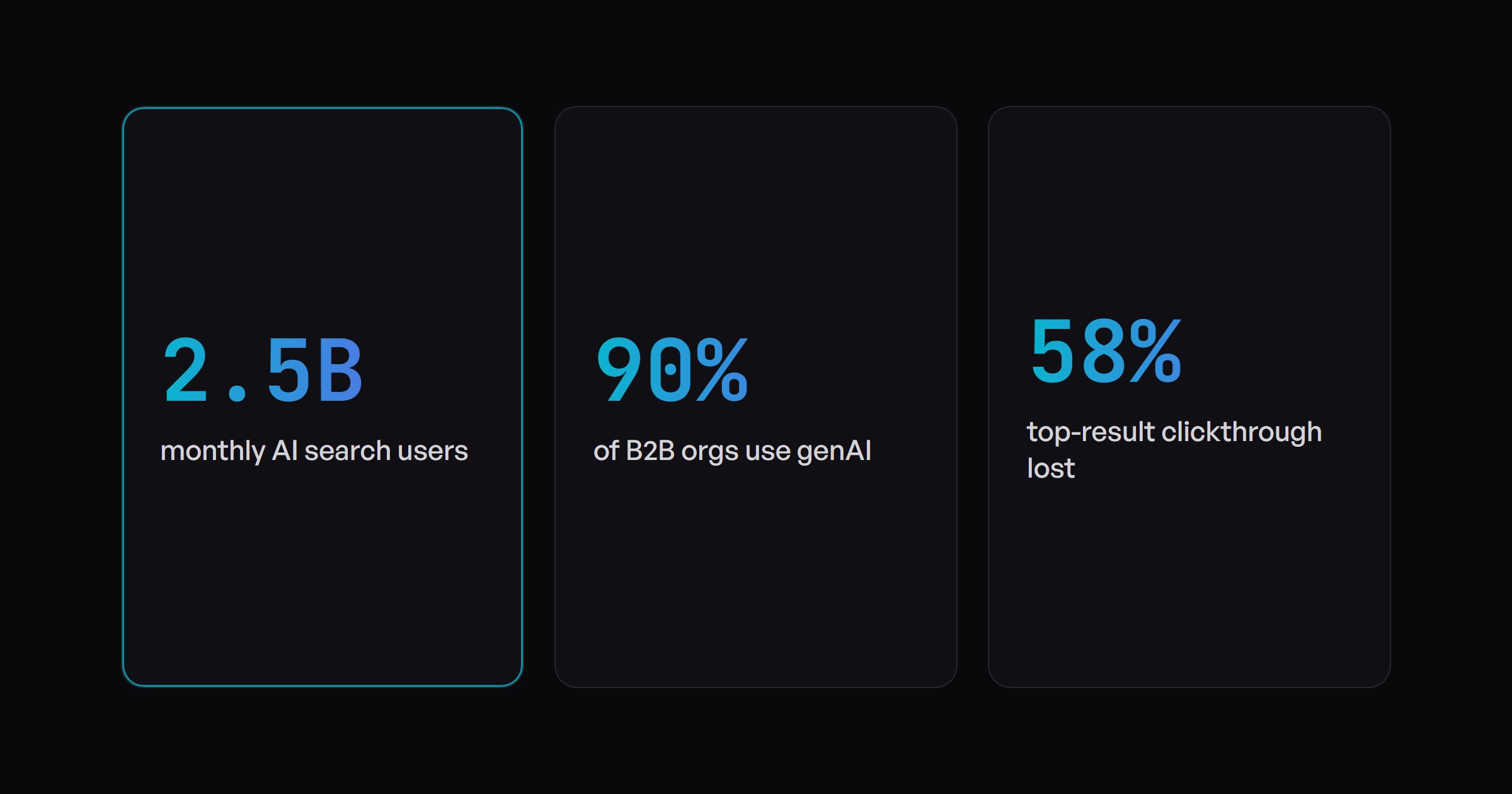

- AI search adoption is no longer a forecast: Google reports 2.5 billion monthly users on AI Overviews and over 1 billion on AI Mode, and independent analysis puts AI assistants at roughly 56% of global search engine volume.

- B2B is ahead of the curve, not behind it. Forrester finds 90% of organizations already use generative AI in their purchasing process, and B2B buyers adopt AI search at three times the rate of consumers.

- Visibility has decoupled from traffic: the top organic result loses 58% of its clickthrough when an AI Overview appears, and users click any link in only 8% of visits with an AI summary present.

- The public record covers adoption and click behavior well, but there is still no auditable public dataset on per-category engine mix or citation patterns. Claims at that resolution deserve methodology questions.

- The defensible response is to measure brand presence inside AI answers directly, in one's own category, where the results can be checked against the engines themselves.

Adoption is no longer the open question

The scale numbers stopped being interesting as predictions and started being interesting as baselines.

At I/O 2026, Google reported that AI Overviews now has over 2.5 billion monthly active users, and that AI Mode passed 1 billion monthly users within a year of launch. The velocity matters more than the totals: in July 2025, AI Mode counted roughly 100 million monthly users across the US and India. A tenfold jump in under a year is not a feature finding its audience. It's a default behavior forming.

Outside Google, the picture is the same. A March 2026 analysis by Graphite.io, reported by Search Engine Land, estimates AI tools now generate 45 billion monthly sessions worldwide, about 56% of search engine volume, with ChatGPT representing 89% of global AI sessions. The same study notes most of that activity happens in mobile apps, which is one reason it stays invisible to teams watching web analytics.

None of these figures says anything about any individual brand. What they establish is that the channel is no longer optional to understand. The question left is who shows up in it.

B2B buyers moved first, and faster

The lazy assumption was that AI search is a consumer phenomenon that would reach B2B eventually. The data says the opposite happened.

Forrester's Buyers' Journey research, reported by Digital Commerce 360 in July 2025, found that 90% of organizations now use generative AI in some aspect of their purchasing process, and that B2B buyers are adopting AI-powered search at three times the rate of consumers. The same report measured AI driving 2% to 6% of total B2B organic traffic, growing more than 40% per month.

The mechanics explain why. A B2B evaluation is research-heavy by design: long lists, feature comparisons, pricing logic, integration questions. That's precisely the work conversational engines compress from hours to minutes. A buying committee (Forrester counts 13 internal stakeholders and 9 external influencers in a typical decision) doesn't browse ten vendor sites together. Increasingly, someone asks ChatGPT, Gemini, or Perplexity to draft the shortlist, and the committee debates what comes back.

For a marketing leader, that relocates the most consequential moment of the funnel. The shortlist conversation now happens inside an answer, before the first site visit ever registers.

Visibility has decoupled from traffic

The sharpest finding in the public record is what AI answers do to clicks.

Ahrefs, in a December 2025 update across a 300,000-keyword sample, found that the presence of an AI Overview correlates with a 58% lower average clickthrough rate for the top-ranking page. Pew Research measured the same effect from the user side: with an AI summary on the page, people click a result link in roughly 8% of visits, versus 15% without one. And Gartner's much-cited forecast, made back in early 2024, expects traditional search volume to fall 25% by the end of 2026 as buyers shift to AI chatbots and agents.

Read together, these numbers describe a structural change, not a dip. The answer itself became the destination. A brand can hold the #1 organic position, watch its traffic erode, and conclude the channel is dying, when what actually happened is the buyer got their answer one layer up, in a summary that may or may not have mentioned the brand at all.

That's why session counts and rankings have quietly stopped describing reality. The unit that matters in AI search is presence: whether the answer names the brand, what it says, and which sources it pulled from.

What the public record still can't say

Honesty about the data requires naming its limits.

There is solid public evidence on adoption, on click behavior, and on aggregate engine share. There is no auditable public dataset on the things practitioners most want to know: which engines dominate which buying categories, how citation patterns differ by vertical, or how often a given engine names a given class of brand. The published studies stop at the aggregate level.

That gap is exactly where unverifiable vendor research tends to bloom. When a report claims category-level precision (thousands of queries, hundreds of categories, neat percentage findings), the methodology questions are fair game: who ran the queries, when, on which engine versions, and can the answer corpus be inspected? If the answer is no, the number is marketing, not measurement.

The defensible alternative isn't to wait for a perfect public study. It's to measure the category directly: run the actual buyer questions against the actual engines, on a schedule, and keep the receipts. That's first-party data in the only sense that matters, because anyone can re-run the same prompt and check it. It's also the approach behind how Zumi monitors brands across nine engines daily, and it's checkable by design.

What to do with six numbers

A practical reading of the mid-2026 record, for a team that owns a brand's pipeline:

- Baseline presence, not traffic. Run the category's real buying questions through ChatGPT, Gemini, Perplexity, Claude, Copilot, and AI Overviews, and record whether and how the brand appears. That baseline is the number the rest of the work moves.

- Weight the engines by the buyer, not by headlines. ChatGPT's 89% share of global AI sessions is an average across everything. A specific B2B category can look very different, and the mix shifts.

- Treat falling clicks as a measurement problem first. Before declaring a channel dead, check what the AI layer above it is saying. The traffic didn't vanish, the decision moved.

- Hold every stat to the standard in this piece. Named source, date, working link. Content built on attributable data is also, not coincidentally, the kind AI engines cite.

The shift is measured, public, and faster in B2B than anywhere else. The open question is brand-specific, and it's answerable in an afternoon: a free AEO readiness check shows how a site stands today, and a demo pulls the live answers for a real category, no deck required.

Sources

- Google, Sundar Pichai I/O 2026 keynote (AI Overviews 2.5B monthly active users; AI Mode past 1B monthly users in its first year). blog.google

- TechCrunch, "Google's AI Overviews have 2B monthly users, AI Mode 100M in the US and India" (July 2025). techcrunch.com

- Graphite.io analysis by Ethan Smith, reported by Search Engine Land, "AI assistants now equal 56% of global search engine volume" (March 2026). searchengineland.com

- Forrester, Buyers' Journey Survey, reported by Digital Commerce 360, "Forrester: AI search is reshaping B2B marketing" (July 2025). digitalcommerce360.com

- Forrester, "The State of Business Buying, 2026" press release (buying group composition). forrester.com

- Ahrefs, "AI Overviews Reduce Clicks by 58%" update (December 2025, 300,000-keyword sample). ahrefs.com

- Pew Research Center, "Google users are less likely to click on links when an AI summary appears in the results" (July 2025). pewresearch.org

- Gartner, "Gartner Predicts Search Engine Volume Will Drop 25% by 2026, Due to AI Chatbots and Other Virtual Agents" (February 2024). gartner.com